Source: Orion Advisor Services, AlphaGlider

Global investment markets lost their strong momentum from 2025 when US and Israel initiated five plus weeks of aerial attacks against Iran in late February. The global equity market, as measured by the MSCI ACWI IMI Index,^d was down 2.8% during the quarter. The US equity market (S&P 500a) led the downturn, experiencing a 4.4% decline, while foreign developed markets (MSCI EAFEb) fell 1.2% and emerging markets (MSCI Emerging Markets Indexc) dropped 0.2%. Fixed income markets treaded water during the quarter—our fixed income benchmark, the Bloomberg US Aggregate Index,e was down 0.1% during the quarter.

Over the last 12 months, equity returns were especially strong—despite the tumult of two US/Israeli attacks against Iran and President Trump’s “Liberation Day” tariffs. Global equity markets returned just over 20% led by a nearly 30% expansion in emerging market equities. US equities lagged other regions, but still posted a healthy 17.4% gain. Bonds had a solid 12-month performance with our fixed income benchmark increasing 4.4%.

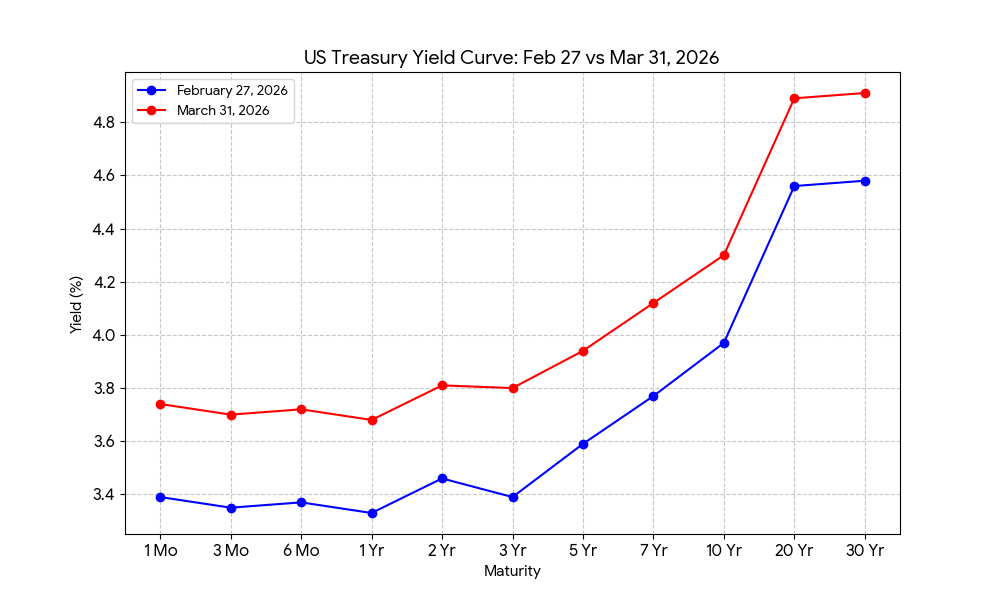

US inflation continues to run well above the Federal Reserve’s (Fed’s) 2% target, with the Fed’s most recent reading of its preferred inflation gauge [Core Personal Consumption Expenditures (PCE) Price Index] rising at an annualized rate of 4.4%. This was through February, before the flow through of higher energy prices caused by Iran’s blockade of the Strait of Hormuz. The worsening inflation picture combined with the Iran war’s negative impacts on the US government’s deficit (earlier this month the White House requested a 40% increase in defense spending, to $1.5 trillion, for fiscal year 2027) have caused investors to reign in their expectation for further Fed rate cuts. As a result, Treasury interest rates across all durations expanded significantly during the month of March, as shown below.

Source: Google Gemini (AI)

Today’s rising rate environment is occurring despite Trump’s late January nomination of Kevin Warsh to lead to Fed when Jerome Powell’s term ends in mid-May. Warsh is a former Fed governor with a history of advocating for rate increases when Democrats are in power, and rate decreases when Republicans are in power. Right on cue, Warsh has recently criticized the Fed’s hesitancy to lower rates further, arguing that AI-driven productivity gains can sustain economic growth without reigniting inflation. With inflation and deficits on the rise, the market seems to doubt Warsh’s ability to convince a majority of his 11 fellow voting members on the Federal Open Market Committee (FOMC) to lower Fed rates, at least in the short term. And although Warsh is considered an experienced and qualified economist, his nomination may not occur before mid-May if the Department of Justice continues to pursue its criminal investigation into Powell’s handling of Fed headquarters renovations. Thom Tillis, the North Carolina Republican Senator on the Senate Banking Committee, is refusing to advance Warsh’s nomination until the investigation, which he considers to be politically motivated by Trump, is dropped.

In February, the Supreme Court ruled 6-3 that all of Trump’s tariffs applied under the International Emergency Economic Powers Act (IEEPA) were unconstitutional. The US government estimated that it collected $166 billion from more than 330,000 businesses in IEEPA tariffs before the Supreme Court’s ruling. A federal trade court judged has ordered the return of these unconstitutional tariffs which will add more strain to the federal deficit. Soon after the Supreme Court decision, Trump announced a new 15% global tariff, invoking Section 122 of the Trade Act of 1974. Section 122 is used to address a balance-of-payments crisis by implementing global tariffs for 150 days, or longer if Congress authorizes it. Many legal experts believe these new Section 122 tariffs are also illegal, but it is unlikely that the US legal system will have time to rule on it before the 150 day period expires. During this window, Trump plans to enact Section 201, 301, and 232 (national security) tariffs to effectively replace the IEEPA tariffs that the Supreme Court struck down. The bottom line for companies around the world, both US and foreign, is that they continue to lack visibility on the rules of trade within the US, hurting and delaying their ability to make educated decisions on future investment plans.

Last, but hardly least in importance, is the deteriorating situation in the Middle East. The US and Israel went into this new military campaign against Iran with vague and perhaps unrealistic goals and expectations for what they hoped to achieve. They also went into this action with minimal outreach to or support from their allies. At various times the two countries’ leaders voiced a desire for regime change, to neuter Iran’s ability to field nuclear weapons, and to destroy its navy and inventory of ballistic missiles and drones. After five plus weeks of massive aerial attacks against Iran, the US and Israel have little to show for their efforts.

Israel was able to assassinate Supreme Leader Ali Khamenei in the opening hours of campaign, but Iran quickly replaced him with his second son, Mojtaba Khamenei. Having lost his mother, wife, a child, and perhaps the use of his own legs in the same strike that took his father, Mojtaba would appear to be someone with an unusually strong desire for revenge against his enemies. And after enduring weeks of aerial bombardment and threats to its infrastructure and its very civilization, the people of Iran would now seem to be aligned with their religious leaders—instead of protesting in the streets about economic conditions as many of them were doing in early January. Regime change in Iran would appear to be more unlikely today than at any other time in decades.

Iran’s nuclear facilities have incurred further damage, but the enriched uranium and intellectual know-how to build a nuclear weapon remain in the country. Having negotiated one nuclear deal that Trump pulled out of in his first term, and having been attacked twice by Trump (and Israel’s Benjamin Netanyahu) during negotiations over the last nine months, the Iranian regime could decide that it is safer to follow North Korea’s lead by rushing to build a bomb that would deter future US (and Israeli) attacks.

The US has made some high profile sinkings of larger Iranian naval vessels, but most of Iran’s estimated fleet of 3,000 to 5,000 small, high-speed vessels equipped with anti-ship missiles, rocket launchers, heavy machine guns, and mine-laying equipment remains intact. It is a similar story with Iran’s arsenal of missiles and drones which continued to inflict damage not only to Israel and US military installations in the region, but also against economic targets of US-aligned countries in the region such as Kuwait, Saudi Arabia, Bahrain, Qatar, UAE, and Oman.

As I write this, we are a few days into the two-week ceasefire negotiated with the help of Pakistan. The conversation is no longer about nuclear programs, or free and fair elections. Instead, it is about reopening a body of water that was open before the US and Israel started the war. Iran’s control of movement in the Persian Gulf and through the Strait of Hormuz, with low cost, easily concealed and moveable missiles, drones, and naval mines gives Iran the upper hand in negotiations with the US. Approximately 20% of the world’s oil and gas, and one-third of its fertilizers passed through the Strait before this war began, and now much of it has stopped. The whole world is enduring a massive demand destruction event for these key commodities—forcing prices up to the point where demand falls enough to match the newly reduced supply. Companies and consumers have no choice but to go without or to pay the marginal buyer’s price point. And although the US is the world’s largest producer of oil and gas, this only benefits the small sliver of its economy that produces this energy. The rest of the economy, including you and me and most of the US companies we invest in, pay the same inflated price that the rest of the world pays. What we are witnessing are the beginning stages of stagflation—rising prices and interest rates denting growth and eventually employment. There are few winners from this situation other than Russia and large oil and gas companies operating outside of the Middle East.

PERFORMANCE DISCUSSION

First Quarter

During a quarter in which the S&P 500 fell -4.4% and aggregate US bonds were flat, all AlphaGlider Core strategies returned a small positive total return. Their quarterly outperformance relative to their respective benchmarks was one of their best in AlphaGlider’s 13-year history—between 2 and just over 3 percentage points, with our more aggressive strategies performing at the higher end of this range. This outperformance was achieved both before the Iran war, and during the month of March. Our ESG strategies also outperformed their benchmarks, but to a lesser extent than our Core strategies due to their lower exposure to the fossil fuel sector and to their slightly higher expense ratios.

Our strategies benefitted from their small relative underweight position in equities, but more importantly, it was the mix within their equities that helped drive relative performance during the quarter. Our underweighting of US equities helped us in general—but it was our large underweighting of US large cap growth stocks, particularly those in the technology and communications sectors, that helped even more. And although we were underweight US stocks, we were actually overweight US small cap, mid cap, value, and quality stocks, which all held up relatively well during the quarter. Our strategies also benefited from their overweight position in foreign developed markets. As in 2025, it was our large overweight positions in the South Korean, Taiwanese, and Japanese equity markets that were especially rewarding for our strategies this quarter.

Our strategies’ positions in the fixed income markets also helped relative performance during the quarter, notably our overweighting of short duration, corporate, and inflation-indexed bonds. Our long/short US equity fund, which we use as an alternative to fixed income, returned a solid 6% gain during the quarter. Our general commodities fund did its job to offset the negative impact on fixed rate bonds, rising nearly 25% during the quarter.

Although our more aggressive ESG strategies missed out on strong performance from the fossil fuel sector, they did benefit from renewed interest in clean energy alternatives. Our dedicated clean energy fund was up 11% during the quarter.

As with most diversified portfolios, we did have some detractors to our relative performance during the quarter. Our emerging market and foreign developed bond funds declined approximately 2%. And our mild underweighting of energy-related equities in our Core strategies, and significant underweighting in our ESG strategies, also dragged on performance.

Last 12 Months

AlphaGlider Core strategies put up strong absolute and relative performance over the last 12 months. All strategies delivered double-digit returns with our most aggressive strategies (AG-A & AG-A/esg) breaking the 20% level. AlphaGlider Core strategies outperformed their respective benchmarks, by approximately 10-15%, while our ESG strategies slightly outperformed their benchmarks.

As in Q1, our strategies benefited from their overweighting of foreign equities at the expense of US equities over the last 12 months. In particular, it was our outsized positions in Asian markets like South Korea, Taiwan, and Japan that made a large beneficial impact. Our overweight position in US small cap stocks also helped during this period. Our more aggressive ESG strategies benefitted from their exposure to clean energy equities.

Within fixed income, our emerging market and domestic mortgage-backed securities performed well. Our alternative investments, general commodities and long/short US equity, also rang up strong returns over the last 12 months.

On the negative side, our strategies missed out on some of the strong performance from US growth, and US large cap technologies stocks in particular, over the last year. Likewise, our underexposure to the US energy sector and our overweighting of US quality, value, and mid-cap stocks also held back 12-month relative performance.

On the fixed income side, our overweight positions in foreign developed bonds and inflation-protected Treasuries were detractors over the last 12 months.

LOOKING FORWARD

After Trump announced his ‘Liberation Day' tariffs last April, we made several changes to AlphaGlider strategies to lower exposure to the US dollar, US bonds, Chinese equities, and US small caps, and to raise exposure to international bonds, commodities, and non-Chinese emerging markets. On the whole, these changes played out well for us in the lead-in to Iran War, particularly over the end of 2025 and the beginning of 2026. Therefore in late January, we did some portfolio rebalancing to trim some of our bigger winners and buy more of some assets that had not kept up. In general, this meant selling equities (particularly international equities) to buy bonds. As some of our bigger winners were only first bought last April (e.g. non-Chinese emerging market equities and general commodities), we elected to delay some rebalancing in taxable accounts until we reach the 1-year anniversary of their purchases, qualifying those clients for a lower capital gains tax rate. We also made several small changes to our strategies, as explained below:

Lower US dollar exposure

We were bearish on the US dollar for several reasons. Although the US dollar index (DXY)f had fallen 5% since last April, it was still 10% above its 20 year average. Through his military and economic threats against both friend and foe, Trump continued to stoke the "sell America" impulse of global markets. And Japanese investors, who hold over $5 trillion in US equities and bonds, are also increasingly motivated to pull money from the US as their local bond yields had finally rebounded to attractive levels after 25+ years, in addition to their currency hitting 40 year lows. In the short term, we thought we could see the dollar suffer from yet another US government shutdown by the end of the January as Congressional Democrats demanded changes to Trump's aggressive immigration enforcement policies. Additionally, Trump said that he was comfortable with the dollar's decline since he retook office, and in fact he thought "it's great" for US exports, giving a green light for markets to continue selling the dollar without fear of US monetary intervention.

We reduced our US dollar exposure by trimming our ultra short-term Treasury and our short-term inflation-protected Treasury (TIPS) positions. We also increased our holdings in general commodities and non-hedged international bonds, both likely beneficiaries of a declining US dollar. In hindsight, our timing to further decrease our dollar exposure could have been better—the “safe haven” dollar rebounded strongly when the US and Israel launched its attack on Iran only a month later.

Lower exposure to US government inflation readings

Trimming our short-term TIPS position also had the benefit of reducing our exposure to US government inflation readings. We were growing more skeptical of the accuracy and integrity of government economic statistics—which directly impact the returns on our large TIPS position (their return includes an inflation adjustment). Trump has tirelessly indicated his desire for lower interest rates (which lowers the interest that the government and consumers pay), so much so that he has pressured the Fed to lower rates by attempting to fire Fed Governor Lisa Cook based on unsubstantiated claims of mortgage fraud, and launching a criminal investigation into Fed Chair Jerome Powell. If Trump is willing to so blatantly threaten the all-important independence of the Fed to lower rates, we think it is well within his character to manipulate inflation statistics if given the chance. He cut the budget of the department that measures inflation, the Bureau of Labor Statistics (BLS), and in a literal case of shooting the messenger, he fired its commissioner after a disappointing jobs report. Trump initially tried to install a partisan and unqualified replacement as BLS commissioner, but members of his own party refused to consider his nomination.

Reduce developed Asia exposure, increase China exposure

With the strong run-up in the South Korean, Taiwanese, and Japanese equity markets, and the relative underperformance of the Chinese equity market, we trimmed our developed Asia Pacific and our emerging markets ex-China funds. We put the proceeds into our general emerging markets fund that includes a significant weighting to Chinese equities.

In total, these changes modestly increased fund management fees, with our more conservative strategies seeing the largest rise and our more aggressive strategies seeing the smallest. AG-C saw a ~1 basis point increase to 6.6 basis points (0.066%) and AG-A saw a ~0.25 basis point increase to 5.6 basis points (0.056%).

Vanguard Fee Reductions

The Vanguard Group is by far the largest supplier of funds to AlphaGlider Core strategies. Unburdened to deliver an operating profit to its shareholders (Vanguard is owned by its funds’ investors, i.e. you and me), it is able to undercut most of its for-profit competitors in the fund fees it charges. In turn, their low cost attracts even more investors which builds more scale, allowing it to lower those fund fees further — creating a virtuous growth cycle. Vanguard was at it again in February, reducing fund fees on 84 of it funds, including five that are used in AlphaGlider Core strategies. Over the last two years, Vanguard fee reductions to over 60% of its fund lineup have saved Vanguard shareholders an estimated

$600 million in annual fee reductions.

Minimizing investment costs, be they taxes, advisory fees, or fund management fees, are a critical factor in maximizing your long-term investment returns. Minimizing fund fees has allowed Vanguard funds to consistently outperform most of its competitors’ funds. For example, 84% of Vanguard’s equity funds outperformed their Lipper peer-group averages for the 10-year period ended December 31, 2025 according to LSEG Lipper. Using Vanguard funds for our AlphaGlider strategies is one element in our attempt to deliver the lowest cost investment solution possible.

1% for the Planet

2025 marks the ninth year that AlphaGlider has contributed one percent of its revenue to a nonprofit working to address challenges posed by anthropogenic climate change.

As in the previous year, we made our 2025 donation to Ceres, a nonprofit advocacy organization that is working to accelerate the transition to a cleaner, more just, and sustainable economy. Ceres is unique in that it is one of the few organizations working with investors, companies, and policymakers to build leadership and make the economic case for bold climate action.

NOTES & DISCLOSURES

1This material represents an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete, and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor.

2Mutual funds, exchange-traded funds and exchange-traded notes are sold by prospectus. Please consider the investment objectives, risks, charges, and expenses carefully before investing. The prospectus, which contains this and other information about the investment company, can be obtained directly from the Fund Company or your financial professional. Be sure to read the prospectus carefully before deciding whether to invest.

3Alternative investments, including hedge funds, commodities and managed futures involve a high degree of risk, often engage in leveraging and other speculative investments practices that may increase risk of investment loss, can be highly illiquid, are not required to provide periodic pricing or valuation information to investors, may involve complex tax structures and delays in distributing important tax information, are subject to the same regulatory requirements as mutual funds, often charge higher fees which may offset any trading profits, and in many cases the underlying investments are not transparent and are known only to the investment manager. The performance of alternative investments including hedge funds and managed futures can be volatile. Often, hedge funds or managed futures account managers have total trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor’s interest in alternative investments, including hedge funds and managed futures and none is expected to develop. There may be restrictions on transferring interests in any alternative investment. Alternative investment products including hedge funds and managed futures often execute a substantial portion of their trades on non-US exchanges. Investing in foreign markets may entail risks that differ from those associated with investments in the US markets. Additionally, alternative investments including hedge funds and managed futures often entail commodity trading which can involve substantial risk of loss.

4Rebalancing can entail transaction costs and tax consequences that should be considered when determining a rebalancing strategy.

5AlphaGlider LLC does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstance.

^Indices are unmanaged and investors cannot invest directly in an index. The performance of indices do not account for any fees, commissions or other expenses that would be incurred.

aThe Standard & Poor's 500 (S&P 500) Index is a free float-adjusted market capitalization weighted index that is designed to measure large cap US equities. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization in the US equity markets.

bMSCI Europe, Australasia and Far East (EAFE) Index is a free float-adjusted market capitalization weighted index that is designed to measure the investable universe of developed market equities outside of the US.

cMSCI Emerging Markets (EM) Index is a free float-adjusted market capitalization weighted index that is designed to measure large and mid-cap equity market performance in the global Emerging Markets.

dMSCI All-Country World (ACWI) Investable Market Index (IMI) is a free float-adjusted market capitalization weighted index that is designed to measure the investable universe of global equity markets.

eThe Bloomberg Barclays US Aggregate Bond Index is a market capitalization weighted index that is designed to track most investment grade bonds traded in the United States. The index includes Treasury securities, government agency bonds, mortgage-backed bonds, corporate bonds and a small amount of foreign bonds traded in the United States. Municipal bonds and Treasury Inflation-Protected Securities (TIPS) are excluded due to tax treatment issues.

Copyright © 2026 AlphaGlider LLC. All Rights Reserved.

No part of this report may be reproduced in any manner without the express written permission of AlphaGlider LLC.