Active management or low fees?

Yes. :-)

The big problem with active investment management is its costs usually outweigh its benefits. But not so with AlphaGlider. Our low cost structure and our use of highly liquid indexed exchange-traded funds (ETFs)1,2 and mutual funds allow us to deliver experienced, professional active investment management, and low fees.

These are three key elements of our investment philosophy:

Active at Our Core

We are firmly in the camp of Robert Shiller, the 2013 Nobel Laureate in Economic Sciences. While asset price moves are next to impossible to predict in the short-term, they are fairly predictable over the long-term. Markets periodically act irrationally and inefficiently, driving asset prices well below or above their intrinsic values.

We are patient, disciplined, contrarian investors, seeking to take advantage of the market's short-term orientation. We own the company and we have most of our investments in AlphaGlider strategies. This encourages us to do what is right for the long-term growth of our strategies, instead of hugging indices1 and following "the herd" to avoid career risk. We strongly adhere to valuation metrics which are successful over long time periods, patiently watching for fear in the markets to serve up attractive investment opportunities.

Passive in Our Tools

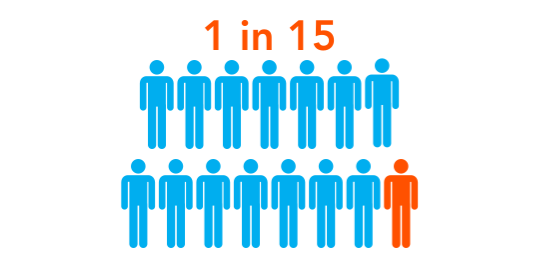

The ratio of actively managed US large-cap core funds that outperformed the S&P 500 over the 10-years ending December 31, 2025, S&P Indices Versus Active Funds (SPIVA®) U.S. Scorecard.

Traditional active investing, that is to say "stockpicking" or "security selection," requires a lot of time, travel, and expertise when done properly. This is expensive, and that's why the field of equity mutual funds had an average fund management fee (i.e. expense ratio) of 1.10% in 2024 (Investment Company Institute, 2025 Investment Company Institute Fact Book, pg. 84). With such high costs, it's no wonder that so few of these funds are able to beat their benchmarks — only 1 in 15 actively managed domestic large-cap core funds was able to outperform the S&P 5003 over the last 10 years ending December 31, 2025 [S&P Dow Jones Indices, S&P Indices Versus Active Funds (SPIVA®) U.S. Scorecard]. And with the tens of thousands of intelligent, highly-educated, and well-paid analysts and portfolio managers all seeking to beat one another, it's no surprise that on average they fall short of their benchmarks by about the amount of their expense ratio. For the case of actively managed domestic large-cap core funds over the last 10 years, this average annualized shortfall was 2.84% vs the S&P 500 (SPIVA® U.S. Scorecard).

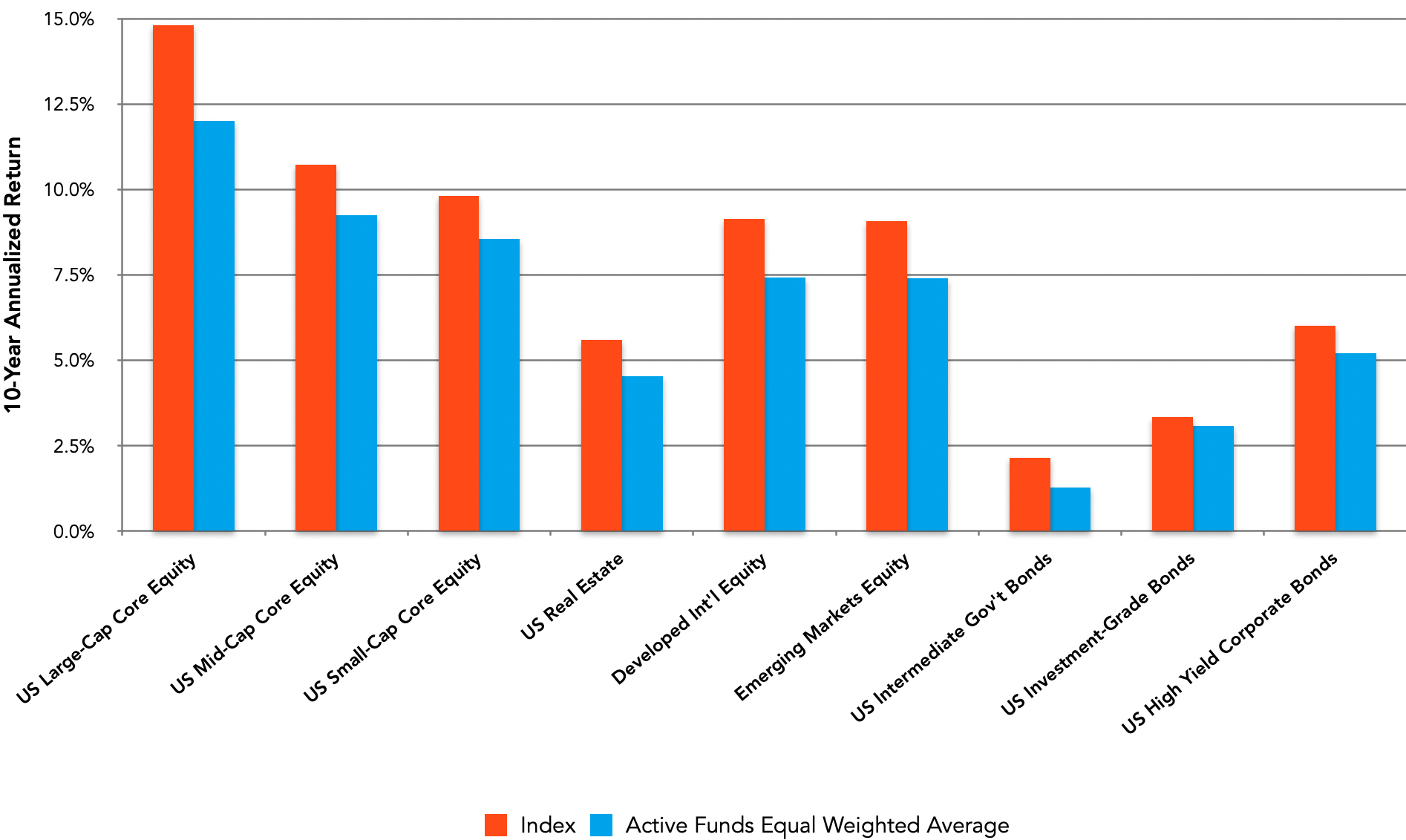

It's not just domestic large-cap core funds which fail to keep up with their respective indexes over long time periods — it's funds in nearly all categories of equity and fixed income. Indexes beat the average actively managed fund in 34 of the 38 fund categories over the last 10 years. Below is a chart showing the results for nine of the larger categories.

10-Year Average Annualized Returns, Active Funds vs Indexes, ending December 31, 2025

Source: AlphaGlider, S&P Indexes Versus Active Funds (SPIVA®) U.S. Scorecard

Much academic literature indicates that asset allocation4 is a more important driver of portfolio performance than security selection. This is fortunate because asset analysis can be performed much more cheaply than security selection. As every dollar saved on investment expenses is a dollar added to investment performance, AlphaGlider has chosen to focus on asset allocation in our attempt to deliver attractive risk-adjusted returns for our clients. We aim to generate positive alpha, that is an investment return above that expected for the level of risk taken, by actively setting our strategies' asset allocations with the use of highly liquid and extremely low cost, passive index funds. We call this being "actively passive."

Diversified and Rebalanced as a Rule

It is said that diversification4 is the only "free lunch" in the financial markets. The free lunch comes from the ability to increase expected returns without increasing the level of risk by adding securities to one's portfolio that are not perfectly correlated with one another. AlphaGlider strategies are highly diversified across asset classes, geographies, industry sectors, market capitalization, and investment style.

We continuously monitor your portfolio's composition, and rebalance5 it whenever its mix of assets strays too far from its target allocation. Rebalancing helps prevent your portfolio from acquiring different, unwanted risk-return characteristics.

Although the primary purpose of rebalancing is to minimize risk, it can also improve risk-adjusted returns. Vanguard research (pg. 13) has shown that annual rebalancing can add up to 0.35% of additional return each year on average relative to a non-rebalanced portfolio with similar risk characteristics. Rebalancing effectively serves as a non-emotional process to buy assets that performed poorly on a relative basis (buy low) and to sell assets that have performed well on a relative basis (sell high).